Whatever It Takes 2.0?

Axel Merk, Merk Investments April 8th, 2014 If you are convincingly irrational the market may expect extreme measures and front run your bluff. It’s in this spirit that ECB President Draghi is threatening the market with another bazooka. We discuss implications for investors.

During the ECB press conference on April 3, 2014 the official ECB Twitter account tweeted (“GC” is the Governing Council, akin to the FOMC in the U.S.):

In fact, the entire press conference appeared focused on convincing the market that inflation in the Eurozone must move higher. Draghi argues that low inflation is a problem for a couple of reasons:

A key culprit for the low inflation? The euro. He said the exchange rate “is an increasingly important factor in our medium-term assessment of price stability.” A month earlier, on March 6, 2014, Draghi quantified the euro’s drag on inflation:

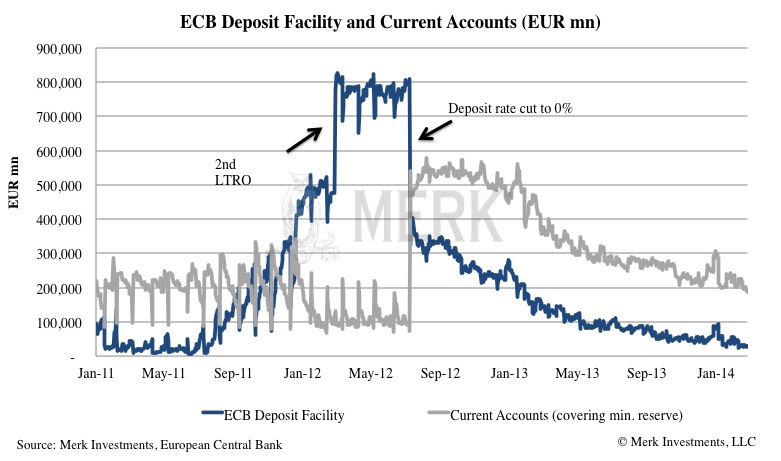

If there was one thing puzzling about the euro last week it was that Draghi’s salvos did not get the euro to plunge. As has happened many times over the past year, Draghi’s verbal assault on the euro didn’t convince the markets. That’s despite threatening to impose negative deposit rates or to engage in “QE.” Trouble is that these tools may not get the job done. Let’s look at the deposit facility at the ECB first:

What one sees is that the deposit facility is small for central bank standards. The facility under consideration is used by banks- we are not talking about negative rates on mom and pop savings accounts; at least not yet. In our assessment, the key implication of moving to negative rates is reputational risk: Northern European savers may lose the little confidence they have left in the ECB if their savings are explicitly robbed. A key role of a central bank is to foster confidence in a currency. Well, in this case, if the ECB wants to weaken the euro they may want to do quite the opposite but we caution policy makers that they are playing with fire. Policy makers, however, are concerned with the opposite risk: that low inflation is causing a revolt in weaker Eurozone countries where negotiating wages downward is incredibly painful. Then there is QE (quantitative easing). Most are not aware that the ECB has operated very differently from the Fed. Rather than “printing” money to buy securities, the ECB has provided liquidity against collateral. The key difference is that ECB facilities expire and banks have returned liquidity they don’t want. Draghi phrases the difference this way:

He realizes that US-style QE doesn’t work in the Eurozone (emphasis added)

With weak demand in the economy and an impaired banking system holding back growth, what could QE do? Draghi may not be able to boost real demand but he is certainly trying to address the impaired banking system. He has been asked in the past why he conducts the stress tests when such tests might discourage banks from borrowing money from the ECB (as this admits weakness); Draghi correctly points out that weak banks don’t lend whether stress tests are conducted or not. As such, it’s important to identify weaknesses; then have a plan to address them. Note that Draghi is actually quite positive on aspects of credit growth in the Eurozone:

To us this suggests the biggest problem appears to be a lack of patience at the ECB. This is confirmed by Draghi’s own words that low inflation isn’t really a problem as it was due to lower food and energy prices – considered transitory and irrelevant by the Fed (at least when they go up!):

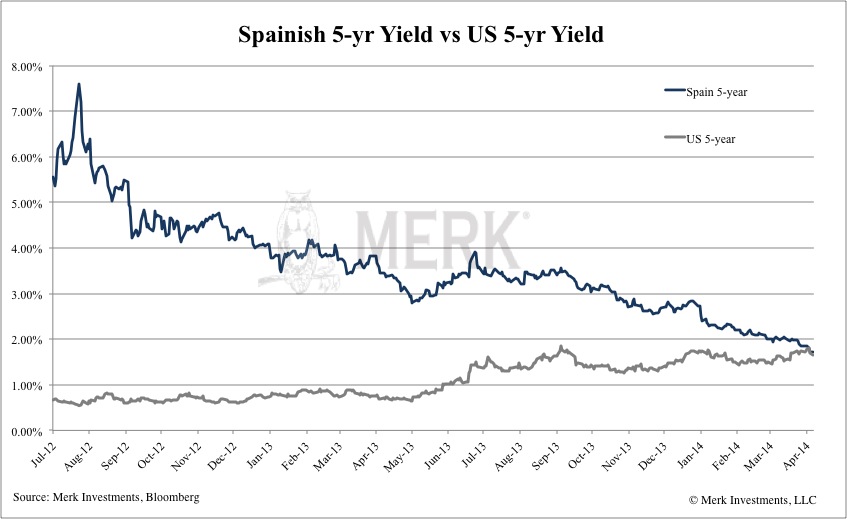

At the other end of the spectrum QE is supposed to increase bond prices to lower yields. In the Eurozone it’s the cost of borrowing of weaker countries (the “periphery”) that matters. I’m not sure how many are aware that the cost of borrowing for Spain for 5 year money is now just about the same as it is for the U.S.:

Draghi’s “whatever it takes” attitude has made peripheral debt securities in the Eurozone appear to be low risk. As such, the flight out of emerging market bonds didn’t make it back to the U.S. but instead to the European periphery. So what exactly should QE achieve if the verbal intervention has already lowered the cost of borrowing; de facto providing a substantial stimulus to the Eurozone periphery, even as ECB short-term rates have only been lowered marginally. Draghi, never short of ideas, wants to improve the “bank-lending channel.” What follows is our own interpretation of what he is planning as he has only provided hints. Last year he referred to an “Asset Backed Securities” (ABS) program to ignite lending in the Eurozone. You may recall ABS as playing a key role in the financial crisis, however, not all ABS are evil. The goal would be to make the Eurozone economy less dependent on banks and more dependent on the markets. If one can securitize debt, credit could flow. Here’s what Draghi said about ABS last week:

We see two key challenges:

However, Draghi may not see these as a problem. That’s because, just like the OMT (Outright Monetary Transaction) program that turned around the fortune in the Eurozone after being announced in August 2012, this may never be implemented. Draghi may hope that the very fact that it is on the drawing board, will convince the markets that credit spreads should tighten and financing conditions should improve for private sector borrowers. What does it all mean? In a nutshell:

For more on how these dynamics may play out, as well as implications for the dollar and gold, please register to be notified when we hold a webinar; our next Webinar is Wednesday, April 16, 2014. Also don’t miss another Merk Insight by signing up for our newsletter. Axel Merk

|