Why I Sell the Dollar: From Dollar Strength to Dollar Weakness

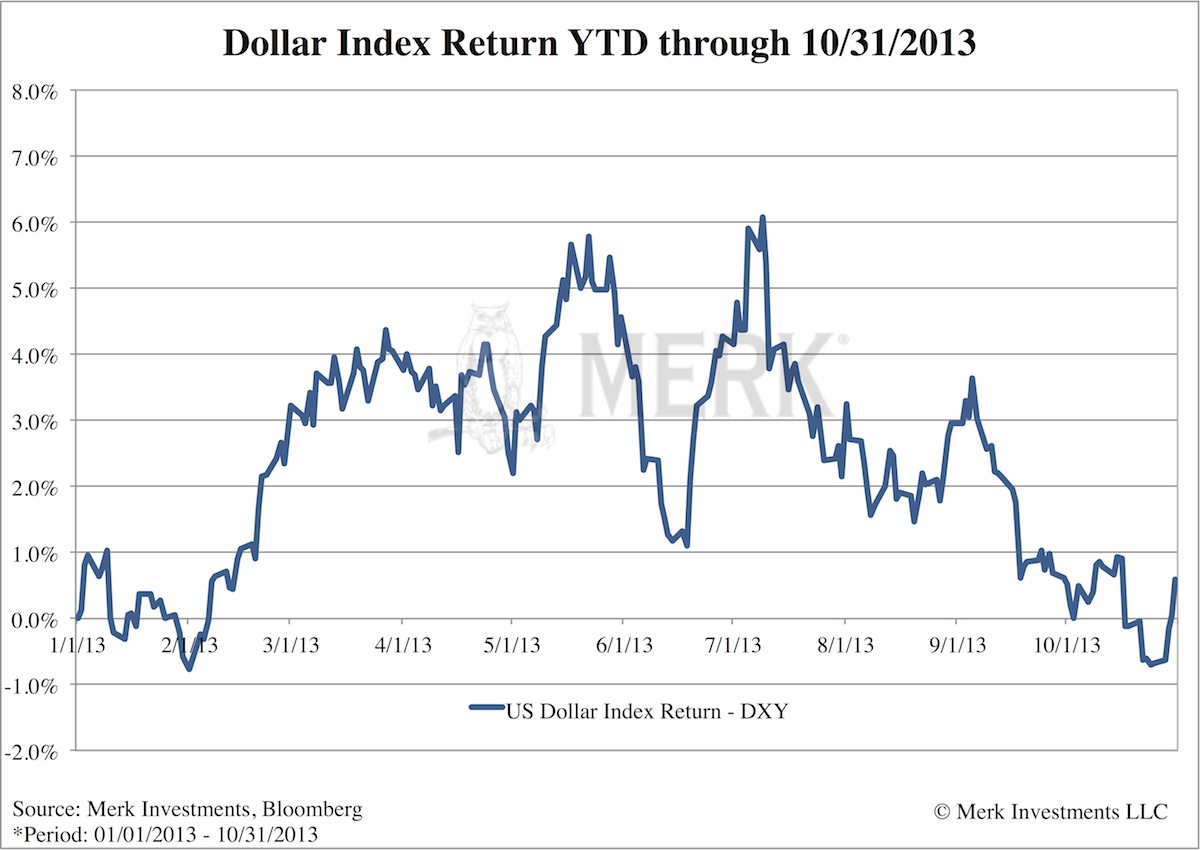

Axel Merk, Merk Investments November 12th, 2013 Q3 of 2013 marked a peak and reversal of direction for the dollar. The notable strength in the dollar during Q2 turned into an equally prominent weakness in Q3 compared to a basket of foreign currencies. All of the G10 currencies strengthened against the dollar during Q3, while the price of gold rose more than 7%. See attached chart for the performance of the U.S. Dollar Index for the year through 10/31/2013.

Euro, the Undiscovered Rock Star In our outlook at the beginning of this year we predicted the euro might become the Rock Star of 2013. When the currency pulled back in the spring, we clarified it might be a rocky ride to stardom (see our analysis “Chaos Investing Unplugged”). By October, the euro gradually climbed back and topped 1.38 in October. While there is still a widespread perception that the common currency of Europe is fairing poorly, in reality the euro was the best performing G10 currency as of this writing, year to date versus the dollar. Why do people believe the euro is going down? We think it may have to do with the misconception that economic recovery and currency performance necessarily go hand in hand. In our analysis, however, not all currencies are created equal. To illustrate the point, consider the yen: the more dysfunctional the Japanese government was (a dysfunctional government is unable to spend money or exert pressure on the central bank), the stronger the yen appeared to be despite the lack of economic growth. In fact, the yen soared higher in early 2011 when the earthquake caused the devastation in Fukushima; a few weeks later, Christchurch in New Zealand was hit by an earthquake, causing the kiwi (New Zealand dollar) to fall. A shock to each economy, causing consumers in the immediate aftermath to spend less and save more. The reason we believe everything appeared to work “backwards” in Japan was because of the country’s current account surplus: as the country was not dependent on foreigners to finance its budget deficit, the expected urge to save by the Japanese exerted upward pressure on the currency. In contrast, the kiwi suffered as foreigners might be less inclined to invest in the country in the immediate aftermath of the earthquake. This is an oversimplification, but is meant to illustrate the point that currencies react differently in different countries to certain economic indicators. The Eurozone, on that note, has a small current account surplus; as a result, we believe, the euro can thrive even in the absence of economic growth. Differently put, other factors such as prevailing monetary policy may have a much stronger impact on currency moves. Alas, while the European recovery is painfully slow, it relies more on structural reforms and less on accommodative monetary policy. Specifically, the euro has benefitted from a shrinking European Central Bank (ECB) balance sheet from early Long Term Refinancing Operations (LTRO) repayments as well as subsiding fears about negative deposit rates hinted at by the ECB earlier in the year. While the ECB just recently and unexpectedly cut its policy rate over disinflation concerns, in our assessment, the ECB has less flexibility than other central banks, particularly the Fed, in implementing policies that would weaken the currency. The most powerful driver behind the euro may be that it is attracting risk-friendly capital, yet did not participate in the rally of recent years that pushed other so-called risk-friendly assets (such as U.S. stocks to name just one) to the stratosphere. This may sound technical, but consider that many that sold emerging market local debt securities are now buying fixed income instruments issued by peripheral (weaker) Eurozone countries. The previous generation of investors that mistakenly thought peripheral Eurozone securities were safe have fled; the new generation is willing and able to take on the risks associated with the securities. We are not suggesting that those securities are suddenly safe, but the risk of “contagion” is dramatically reduced as risk-friendly investors allow risk to be priced locally; in contrast, when an institution deemed too big to fail has significant exposure to risky assets, the fear of contagion can cripple the entire region. As proof, look at Cyprus: during the peak of the crisis, Spain had a Treasury auction where the country paid the lowest yield since the early 1990s. The market is letting us know that a crisis in the Eurozone is not the same as a crisis in the euro. In summary, we believe the euro can be strong, while the European economy is still relatively weak. Dollar, Out of the Frying Pan, Into the Fire The situation in the U.S. is almost the opposite: the true problems (read entitlement spending and government debt) have not been addressed, rather, the economic recovery is dependent on accommodative monetary policy by the Federal Reserve (Fed), taking the country out of the frying pan, and into the fire. Asset bubbles may be forming, but no real reform has been undertaken. Notable is that the dollar is almost flat for the year on the popular U.S. Dollar Index, retracing almost all of its earlier gains. In the mean time, market expectations continue to shift towards a longer time frame for QE. It is the lack of willingness to slow the pace of extreme accommodation that might become of increasing concern to the market. There are two main elements to accommodative policy by the Fed, one is the QE program; the other is the Fed Funds rate, the short-term interest rate that the Fed controls, and the forward guidance that they provide on that rate. In our view, the Fed Funds rate is the more important piece of the puzzle for currency markets, and the decision not to taper is indicative of how cautious the Fed may be in raising rates and how much they will err on the side of keeping policy extremely loose. Given this, while the dollar may experience short-term strength from time to time, as is being evidenced this month, our medium to long-term outlook on the dollar remains bearish. Next February’s change of guard at the Fed should support our case, with Janet Yellen as the über-Dove at the helm. Yen: Headwinds Aloft The yen weakened significantly through the late spring. Since May the yen has been in a trading range consolidating around 98. Despite the dollar strength witnessed for the first part of the year, the yen was not able to meaningfully rally. This is a bad sign for the yen, which will face a myriad of fundamental headwinds over the medium to long term. As a result, we remain bearish on the yen and would not count out a sharp sell off back to the weakest levels seen earlier in the year. Golden Opportunities? Gold fell substantially during Q2, then rallied 7.65% through Q3 coming off of what appeared to be depressed levels under $1,200 per ounce in late June. In our assessment, long term fundamentals for gold remain largely intact. In addition, Gold’s low correlation with other asset classes as well as with other currencies makes it a valuable diversifier. An actively managed currency basket including gold may provide improved risk-return benefits to a portfolio, as it may be able to benefit from gold’s upside potential, yet manage its volatility due to gold’s low correlation with other currencies. Asian Currencies, Best of the EM After several months of relative calm, volatility is likely to resurface in EM currencies, and the market will refocus on individual currencies’ fundamentals. One lesson investors may have learned this year is that currencies of EM countries with fragile external positions are exposed to high liquidity risk when investors rush for the exit. In contrast, most Asian countries, with the notable exception of Indonesia and India, have current account surpluses and modest to large foreign reserves, making the respective currencies more resilient to potential capital outflows. Moreover, the majority of Asian currencies have historically exhibited lower volatility and less exposure to liquidity risk, adding to the factors indicating that Asian currencies may provide investors better risk-adjusted returns compared to other EM currencies. Renminbi on Long, Slow Race Without much fanfare, the Chinese currency has hit a 20-year high against the dollar. We believe Chinese policymakers may continue to allow the currency to appreciate to help mitigate domestic inflationary pressure. Over the long term, we believe the currency may outperform, partly driven by China’s transition to a higher value added and more consumption-oriented growth model. For the renminbi, this is a marathon, not a sprint, which the Chinese tortoise may ultimately win over the American hare. Why Invest in Currencies? To those that say the U.S. has the cleanest of the dirty shirts, we would like to point out that it hasn’t helped the greenback, as evidenced by the euro outperforming the dollar both so far this year, as well as last year. Yes, we have a mess in the Eurozone that won’t be resolved anytime soon. But we also have a mess in the U.S., Japan, and many other places around the globe. Most of these problems are neither new, nor are they going to go away. We may not be able to convince policy makers to pursue sound policies, but we can allocate our money in a way that potentially mitigates some of the risk and provides profit opportunity from what may lie ahead. More specifically, with policymakers staying engaged, asset prices appear to no longer reflect fundamentals, but instead reflect the next perceived move of government policymakers. As such, we believe the currency markets may be a great way to express one’s view of what we call the “mania of policymakers,” as currency movements may provide a more direct reflection of what policy makers are up to. We continue to see numerous opportunities within the currency asset class, and believe that currencies may provide valuable portfolio diversification benefits and upside potential. Please subscribe to Merk Insights and follow me on Twitter for more analysis. Axel Merk

|